No Ceasefire. Day 20. The Cost Is Coming Home to Australia

The Middle East war has now lasted three weeks with no end in sight. The economic impact on Australian freight, fuel, farming and food is no longer distant. It is here.

The conflict that began on 28 February 2026 has entered its third week. There has been no ceasefire offer. There has been no ceasefire request. The Strait of Hormuz remains effectively closed to Western commercial shipping. And in Australia, the consequences are now hitting every layer of the supply chain — from the pump at the service station to the paddock preparing for winter cropping season.

This update focuses entirely on what this means for Australian businesses, Australian farmers, Australian road transport, and every shipment moving in or out of this country.

1. No Ceasefire. What the Diplomatic Position Means for Freight.

The key commercial question for freight is not which side is winning — it is whether the Strait of Hormuz will reopen, and when. On both counts, the picture remains unchanged. Iran's Foreign Minister has publicly stated that no ceasefire message has been sent, and none has been requested. Iran has been explicit: the conflict must end on terms that prevent any recurrence.

At the same time, a growing number of nations are in direct talks with Tehran about safe passage for their own flagged vessels. China, India, Pakistan, Turkey and several others have secured permission-based transits. A small but growing number of non-Iranian, non-Western vessels are now moving through the strait — approximately eight per day as of mid-week, roughly double the figures seen earlier in the conflict. This is significant but far below pre-war transit volumes.

For Australian exporters and importers, the practical implication is unchanged: no Western-flagged vessel is transiting. No Australian carrier operates through Hormuz. Cape of Good Hope rerouting remains the standard for all EU/UK, Indian Subcontinent, Middle East and Africa trades. The extra 3,500–4,000 nautical miles per voyage is locked in for as long as this situation continues.

2. Australia's Fuel Crisis — Diesel Prices, Trucking Costs and National Reserves.

Australia imports more than 90 per cent of its refined fuel. Global oil is priced in US dollars. The Strait of Hormuz handles approximately 20 per cent of the world's daily oil supply. When that corridor closes, the impact reaches Australian fuel prices within days — not months.

What has happened to diesel prices:

• Australian diesel terminal gate prices rose between 29 and 31 per cent across all major capital cities in a single week — from 4 to 10 March 2026. (Source: Australian Institute of Petroleum)

• Sydney, Melbourne, Brisbane, Adelaide and Perth all recorded increases in that 29–31 per cent range within eight days.

• Brent crude oil surged past USD $114/barrel earlier in the month — the highest level since 2022.

• The federal government has declared a fuel supply 'national crisis'. Emergency fuel reserves have been released, up to 762 million litres of petrol and diesel.

• The government has also temporarily lowered fuel quality standards for 60 days, allowing higher-sulphur fuel to be sold — adding approximately 100 million litres per month to the market.

• Panic buying has been reported across regional areas of Victoria, NSW and Western Australia. Some regional towns have run completely out of diesel.

What this means for road transport:

Every container moved between port and warehouse or customer runs on diesel. When diesel prices move 30 per cent in a week, road transport operators cannot absorb the cost. The Container Transport Alliance Australia (CTAA) has advised operators to review their fuel surcharge rates on at least a weekly basis — in some cases daily.

• Industry analysis: every 5 cents per litre increase in diesel translates to approximately 0.7 per cent increase in transport fuel surcharge recovery.

• At current price levels, container transport fuel surcharges are expected to increase materially from mid-March onwards.

• Road transport surcharges are now layering on top of ocean EFS.

For importers taking delivery and exporters moving cargo to port: budget for higher domestic cartage costs. These are not hypothetical — they are already appearing on invoices.

3. Australia's Fertiliser Crisis — The Winter Cropping Season Is at Risk.

This is the most significant downstream consequence of the Strait of Hormuz conflict for the Australian economy that does not involve freight directly. The Middle East is not just a shipping route for Australian agriculture. It is the source of the fertiliser that Australian farmers need to plant their winter crops.

The dependency:

• Australia imported 7.9 million tonnes of fertiliser in 2024 — valued at A$5.5 billion. Of this, approximately 69 per cent of urea imports came from the Middle East.

• Saudi Arabia, the UAE and Qatar combined supplied A$1.1 billion in fertiliser to Australia in 2024 — 42 per cent of total import value.

• More than half of Australia's urea imports originate from the three Gulf states directly affected by the Hormuz closure.

The price impact:

• Urea was trading at approximately A$775/tonne at the start of 2026. By late February, it had reached A$872/tonne.

• After the conflict escalated, the price jumped to A$1,091/tonne by 5 March, then A$1,226/tonne within days — an increase of more than A$350/tonne in a matter of weeks.

• That is a price increase of more than 58 per cent since the start of the year.

The timing problem:

Australia's fertiliser import program typically accelerates from March onwards to position product ahead of winter cropping demand. The next four to six weeks are, historically, the most critical window of the year for securing supply. If Gulf cargoes do not arrive on time, Australia risks both extremely high prices and potential physical shortages during the winter cropping season.

• Qatar was forced to halt production at one of the world's largest urea plants. Nearly one million metric tonnes of fertiliser cargo is reported to be physically stranded in the Gulf.

• Some Australian growers already have open positions for planting fertiliser. Alternative fertilisers such as sulphate of ammonia may be needed if MAP, DAP, urea or UAN cannot be sourced.

• WA growers are already looking to adjust crop mix — potentially less wheat and canola, more barley — in response to price and availability concerns.

• Grain Producers Australia is urging growers who ordered early to recognise their fortunate position. Many others face uncertainty.

If constraints continue, analysts have flagged the potential for costs on perishable goods such as dairy, fruit and vegetables to rise by 40-50 per cent. (Source: former ACCC chair Allan Fels, via Clime Investment Management analysis)

4. Australian Exporters Calling for Government Assistance.

The Freight & Trade Alliance (FTA) and the Australian Peak Shippers Association (APSA) have formally raised the scale of unbudgeted surcharge exposure with government. Their position: significant, unplanned costs arising from shipping disruptions linked to the Middle East conflict are now hitting Australian importers and exporters, and the existing regulatory framework provides insufficient transparency or commercial certainty.

Emergency Fuel Surcharges, war-risk premiums, rerouting costs and extended transit times are all accumulating on Australian businesses simultaneously. For high-volume shippers or businesses with fixed-price customer contracts, the gap between budgeted and actual freight costs is material.

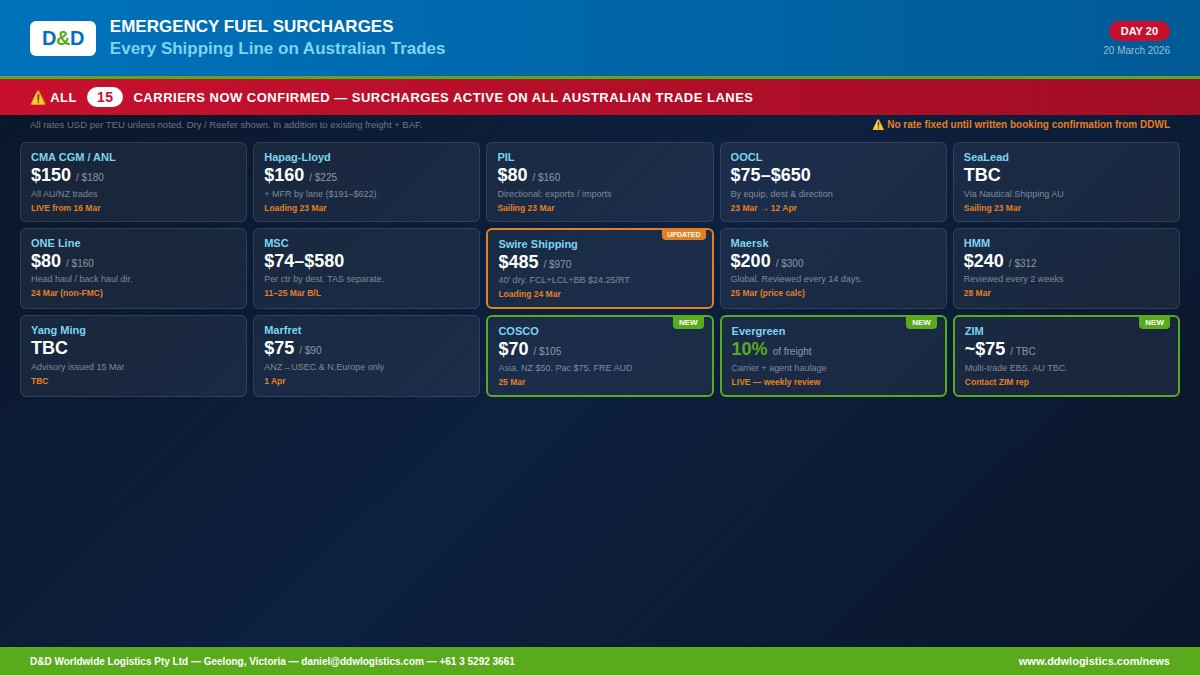

5. Shipping — All Surcharges, All Carriers. Full Updated Table.

As of 20 March 2026, every major shipping line serving Australian trade lanes has either implemented or announced an Emergency Fuel Surcharge. The table below includes all confirmed notices plus status updates on additional carriers.

IMPORTANT:.

* MSC has also introduced updated EFS rates for inbound cargo from Northern Europe and Mediterranean to AU/NZ: USD $200 dry / $300 reefer per TEU (from 16 March). This is separate from and additional to the outbound/NB rate tables previously published.

Carrier | Dry USD/TEU | Reefer USD/TEU | Effective | Notes / Status |

CMA CGM / ANL | $150 | $180 | 16 Mar LIVE | All AU/NZ FCL. First to act. |

Hapag-Lloyd | $160 + MFR | $225 + MFR | 23 Mar | Flat EBS + Marine Fuel Recovery by trade lane |

PIL | $80–$160 dir. | $120–$240 | 23 Mar | Directional: exports $80, imports $160 |

OOCL | $75–$650 NB | $113–$975 | 23 Mar→12 Apr | Officially filed tariff OOLL-100/T-53. 14-day review. |

SeaLead | TBC | TBC | 23 Mar | Trade notice 18 Mar via Nautical Shipping. EBS eff. 23 Mar (sailing date). Rate quantum under review. |

ONE Line | $80–$160 dir. | $105–$210 | 24 Mar | Head/back haul structure. Short Sea $80/$105. |

MSC | $74–$580 NB* | $111–$1,120 | 11–25 Mar (B/L) | Per container by destination. New: N.Europe→AU $200. |

Swire Shipping | TBC | TBC | 24 Mar | RATES CONFIRMED: 20’ dry $485 / 40’ dry $970 (into S.Pacific). 20’ RF $580 / 40’ RF $1,160. BB/LCL: $24.25/RT. Broadest scope of any carrier. |

Maersk | $200 | $300 | 25 Mar | All AU/NZ FCL. Also, air freight surcharge. |

HMM | $240 | $312 | 28 Mar | 2-weekly review — highest flat rate in market. |

Yang Ming | TBC | TBC | TBC | Notice issued 15 March. Rate to be confirmed. |

Marfret | $75 | $90 | 1 April | ANZ→USEC + N.Europe only. BNE 3 Apr, SYD 12 Apr. |

COSCO | EBS eff. 25 Mar | TBC | TBC | EBS confirmed 17 Mar. Asia: $70/$105 TEU. NZ: $50/$75. Europe/Africa: $70/$105. South Pacific: $75/$115. SYD/MEL→FRE: AUD 100/150. Dry/RF. |

ZIM | TBC | TBC | TBC | EBS confirmed across multiple trades. ~$75/TEU historical benchmark. AU-specific quantum pending. Also charges Green Fuel Surcharge (GFS) updated fortnightly. |

Evergreen | TBC | TBC | TBC | No confirmed AU/NZ notice — monitoring. |

TS Lines | TBC | TBC | TBC | Regional carrier. Monitor for notice. |

Quay Shipping | TBC | TBC | TBC | Pacific/ANZ specialist. Monitor for notice. |

NYK / K-Line | — | — | Merged | Merged into ONE Line (2018). Row removed from published article. |

📋 ALL SURCHARGES ARE IN ADDITION TO BASE FREIGHT RATES. No rate is fixed until written booking confirmation is issued by DDWL. All quotes issued before each carrier's effective date do not include the EFS. Call DDWL before booking or quoting your client. |