It's Still Broken. Here's Exactly Where Things Stand. Middle East Conflict — Australian Freight Update | Week of 27 April 2026

I'll be straight with you. A lot happened this week, and most of it didn't go the way people were hoping. We had a brief window where ships were moving through the Strait of Hormuz again. That window lasted about 24 hours. Then Iran seized two more vessels, the blockade tightened, and we're back to where we've been for weeks. This isn't getting resolved before Q3. Possibly not before the end of the year. Here's everything you need to know right now.

The Strait of Hormuz — A Week That Went Nowhere Fast

On 17 April, Iran announced the Strait would open to commercial shipping as part of a Lebanon ceasefire arrangement. Six cruise ships that had been trapped in the Persian Gulf for weeks made it through. For about a day, it looked like a genuine turning point.

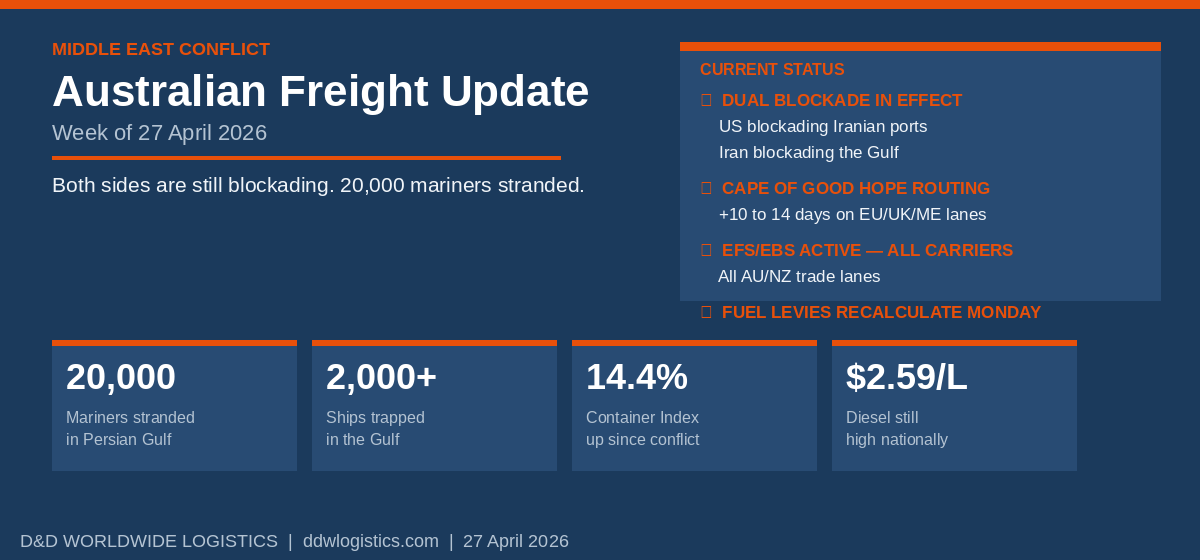

By 20 April, traffic had collapsed again. The International Maritime Organisation reported on 21 April that around 20,000 mariners and 2,000 ships are still stranded in the Persian Gulf. That's the reality of where this is at.

Trump extended the ceasefire on 21 April but kept the US naval blockade locked in. Within hours, Iran's Revolutionary Guard attacked three commercial ships in the Strait and seized two of them. Iran's parliamentary speaker said reopening Hormuz is 'impossible' while the US blockade continues. Iran's Foreign Minister called the blockade 'an act of war.' The US called Iran's ship seizures a ceasefire non-issue because they weren't American or Israeli vessels.

We now have what's being described as a dual blockade. The US is blockading Iranian ports. Iran is blockading the Gulf. Both sides are dug in. Industry analysts are now saying a return to anything resembling normal shipping through Hormuz is months away at best. Goldman Sachs has said publicly that another month of this keeps Brent crude above USD $100 for the rest of 2026.

Iran is reportedly losing around USD $500 million a day with the Strait closed — but analysts believe they have enough oil revenue afloat on tankers to sustain their position through to around August. So don't hold your breath waiting for economic pressure alone to force a resolution.

Military planners from more than 30 nations met at a UK Royal Air Force base this week to design a multinational mission to safeguard the Strait. It's the most significant multilateral response yet. But it won't be activated until there's a sustained ceasefire — and we don't have one.

Cape of Good Hope is the only routing on the Europe, UK, Middle East and Indian Subcontinent lanes. Add 10 to 14 days to all transit times on those trades. There is no Red Sea. There is no Suez. That is not changing soon.

Surcharges — Every Carrier, Every Lane, Still Going Up

Not one carrier has moved to reduce or remove surcharges since the conflict began in late February. Emergency Fuel Surcharges and Emergency Bunker Surcharges remain active across every carrier serving Australian and New Zealand trades. The ANL General Rate Increase I flagged two weeks ago hit on 16 April exactly as announced — USD $350 per TEU and USD $700 per FEU on northern Australian ports: Gladstone, Townsville, Darwin, Dampier and Port Hedland. If you ship through those ports and haven't adjusted your cost models, do it today.

The Drewry World Container Index is sitting at around USD $2,172 per 40-foot container — up 14.4% since this conflict began. Headline freight rates might look stable, but that's a trap. Total landed cost is what's actually going up, and it's going up every week through surcharge stacking — bunker fees, war risk, emergency contingency charges, domestic fuel levies — all layering on top of each other.

Blank sailings on Australian trades are now at 11.9%, up from 9.5% before the conflict. That means missed sailings, port omissions, and less certainty on when your cargo actually moves. If you're working to tight delivery windows, build in an additional buffer.

Freight & Trade Alliance and the Australian Peak Shippers Association have formally written to Prime Minister Albanese, calling for stronger carrier surcharge protections. Australia currently has no regulatory framework to prevent carriers from imposing major surcharges with no notice, sometimes on cargo that's already on the water. The US Federal Maritime Commission has repeatedly blocked carriers from fast-tracking Middle East surcharges without transparency requirements. South Korea has committed AUD $150 million in export voucher schemes to offset conflict-related freight costs for its shippers. Australia offers nothing comparable. That needs to change.

Fuel — A Little Relief at the Bowser. Don't Mistake It for Normal.

There's some genuine good news on petrol. National averages have eased to around $1.89 per litre, well back from the peaks above $2.30 we saw in March. The government's temporary halving of the fuel excise — down to 26.3 cents per litre from 1 April through to 30 June — has contributed. The ACCC has been monitoring closely and has been clear that it expects the full savings to flow through to the pump.

But diesel is still a problem. National averages are sitting between $2.59 and $2.75 per litre, depending on location. That's still materially higher than pre-conflict levels. International diesel benchmarks dropped 18% week-on-week to 22 April, which is encouraging, but that flow-through to retail takes time, and the structural supply pressure from the Middle East hasn't gone away.

Australia Post lifted its fuel surcharge from 4.8% to 12% on 23 April 2026. That's a significant move from a major national operator, and it tells you everything you need to know about where domestic logistics costs are right now.

Domestic cartage operators across Sydney and Melbourne are flagging ongoing weekly surcharge increases. If you're managing inland freight costs, fuel levies are recalculated every Monday. Your invoice will keep moving until fuel markets stabilise, and that's not happening this week.

On supply: forward import orders are within normal levels, and the Geelong refinery — which had disruptions earlier in the conflict — is expected to return to over 90% of capacity in the coming weeks. The acute supply crisis of March has eased somewhat. But with 87% of Australia's diesel imported and the Middle East supplying a significant share of refined fuel globally, any escalation carries supply risk. We're not out of the woods.

Air Freight — More Expensive, Less Available, Not the Easy Fix

If your first instinct is to switch to air to bypass the ocean delays, get current rates first. Gulf hub capacity is severely constrained — Emirates is running at around 75% of normal, Etihad at 50%, flydubai at 33%, Qatar Airways at just 20%. These hubs handle a large portion of east-west airfreight flows, and 13% of all global air cargo normally transits through the Gulf region.

Jet fuel is sitting around USD $195 to $197 per barrel. Global spot airfreight rates are significantly elevated year-on-year. For routes through the Middle East and South Asia, the increases are dramatic. Air freight is more expensive than usual and comes with less schedule certainty. Use it only where the lead time genuinely demands it — and get a quote before you assume it works.

Fertiliser and Food — The Seasons Don't Wait for Diplomacy

The UN flagged last week that farmers dependent on fertiliser through the Strait of Hormuz are running out of time. Iran and Qatar together supply a significant share of global urea. Australia's spring seeding season requires decisions now, well before planting windows open. If you're in agriculture and you've got fertiliser orders in the pipeline, talk to your supplier about timing and routing today.

For food exporters, the situation on Middle East and North African lanes remains expensive and unpredictable. Red meat, dairy, and grains are all exposed to elevated surcharges, extended transit times, and war risk insurance gaps. P&I clubs that pulled Gulf coverage in early March haven't reinstated it. If your cargo touches a Gulf port in any way, confirm your insurance position with your broker before it ships. That's not something we can cover on your behalf under standard freight documents. It has to be confirmed at your end.

What To Do Right Now

Reset your budget if it was built on late 2025 numbers. The market that was expected this year doesn't exist. Plan for elevated surcharges, Cape routing and extended lead times through the remainder of Q2 and into Q3 at a minimum.

Book early. Preferred sailings are filling ahead of schedule. If you need specific vessel windows or have time-sensitive cargo, don't leave it too late.

Check your insurance before anything moves through a route that touches the Gulf. War risk cover is not automatically in place. Confirm it explicitly with your broker.

If you're not sure what any of this means for your specific shipments, call us. That's what we're here for. Our job is to make your job easier, and right now that means cutting through the noise and giving you straight answers on your freight.

We'll be back with the next update early next week. The ceasefire extension is fragile, and new carrier announcements can land at any time. We're watching it daily.

All rates confirmed at time of booking only. No rate is fixed until written confirmation is issued by DDWL. Fuel levies are recalculated every Monday.